Has anyone found a 529 plan with an investment option that Is close enough to halal that they chose to invest in it? If so what is it and what is the percentage of the gains you have calculated for purification?

For CA 529 the one that seemed least haram was this: https://www.morningstar.com/funds/xnas/tiscx/quote. I checked a couple other state plans but didn’t see anything with less exposure to financials. If you found something better please share!

One thing I was hoping Zoya could tackle in the future was evaluation of mutual funds and how much of the gains are impure.

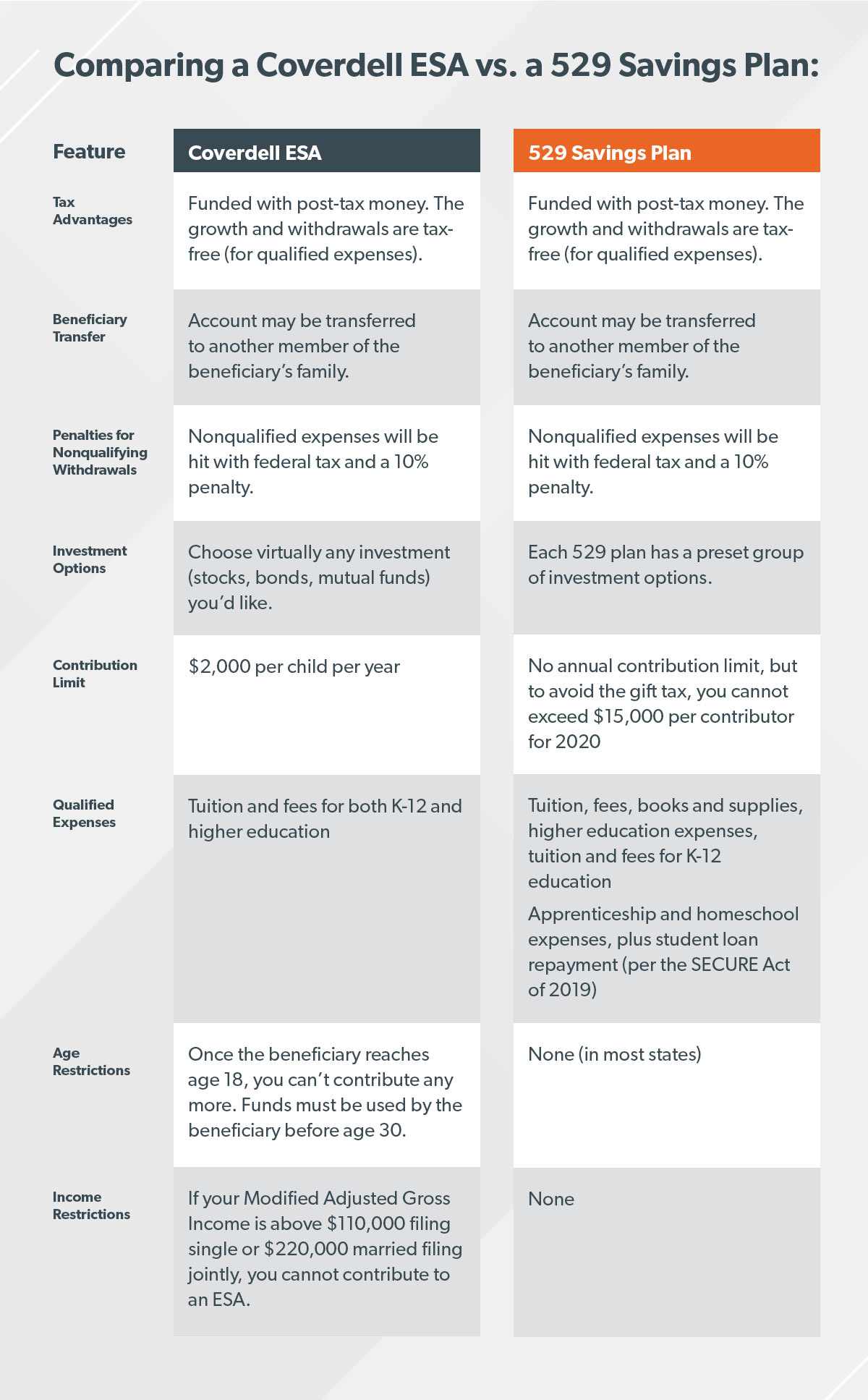

An alternative to a 529 is an Educational Savings Account (ESA). Amana Funds (under Saturna) offers an ESA. The downside of an ESA is that you can only contribute up to $2,000/year. Once it comes time for college/university, the accumulated savings may or may not make a big dent in tuition depending on the school.

If you open an ESA with Amana, you can contribute towards one of their mutual funds (i.e. Income, Growth, Participation). Performance for each fund varies.

After looking at many 529 plans, I decided to open ESAs for my kids. I found that this was the best vehicle to have 100% control over the investments in the accounts.

To my surprise, not all the brokers offered ESAs when I was ready to pull the trigger. I have mines with Schwab.

UTMA/UGMA are custodial accounts that give you the most flexibility of choosing the investments of your choice, such as shariah compliant investments. Downside: 1) It doesn’t get you any tax break and your child pay taxes on liquidation. 2) Once your child turns 18/21, the account gets transferred to him/her, so you don’t have control over what it can be used for.

W’salam,

It’s about the type of investments in a 529 or any other optional investment plan. If you wouldn’t buy those investments outside of the plan because you understand them to not be halal, you probably wouldn’t be comfortable picking them inside the plan.

و عليكم السلام و رحمة الله

The ones I was allowed/ interested in used Bonds as investment vehicles. So that was a non starter.

I recommend checking the 529 plan of interest before pulling the trigger.

Depending on your AGI and the age of your child, it may be best to use a Roth IRA for their education savings. You can pull out contributions to pay for their education and leave the gains for your retirement. If your above the AGI limit, you can use a backdoor Roth.

With the Roth if your child doesn’t go to college or has scholarships etc the money remains yours and is applied towards your retirement.

It all takes a little planning, but the level of control both in what you invest in and what happens to the funds after 18 makes it worth it.

Thanks for that advice. In fact I do have access to add after tax retirement savings that can be automatically converted to a Roth 401K, aside from the standard 401K contributions, and I can invest in halal funds there through Fidelity Brokeragelink. I’ll make use of that inshaAllah. I’m not sure if I can withdraw funds from my Roth 401k but if not I could look into rolling that over into a Roth IRA down the line.

Can we create separate IRA accounts for spouses? Like I have one for myself but can I create one for the wife and contribute to that too? that way we can maximize the contribution to a Roth account?